The US is ‘very far’ behind China and others in creating a national digital currency

Even ahead of President Joe Biden’s White Home Executive Order (EO) very last week, the US had been discovering the generation of a Central Bank Digital Forex (CBDC). But its efforts have fallen far quick of other nations.

In the Executive Purchase, Biden called on several US businesses and regulatory bodies to intensify their exploration of a electronic sort of a dollar, equivalent in some techniques to cryptocurrencies, this kind of as bitcoin, but vastly extra secure. Biden referred to as on the Federal Reserve Process (The Fed) and other oversight bodies to develop suggestions on how to near regulatory gaps, mitigate economic dangers, and handle cybersecurity considerations around cryptocurrency.

At this time, having said that, the US is participating in a video game of catchup with other international locations that are now making use of or piloting CBDCs or electronic tokens. The consquences of the US falling additional beyind could be severe.

“I think the United States has recognized it is extremely far at the rear of other international locations, especially China, which is racing in advance technologically and also plan sensible,” stated Ananya Kumar, assistant director of Digital Currencies at the Atlantic Council’s GeoEconomics Centre, in Washington DC.

“If we never develop our personal, specifications will get established by other international locations by now aware of the benefits of this innovation and the US will be remaining guiding,” Kumar mentioned. “The EO came out extremely strongly for American management on these problems. The US to day has not been concentrating coordinated attempts on this.”

Members of the Atlantic Council, a consider tank, testified right before Congress previous summer time on the deserves and challenges of CBDCs, which are more rapidly, less costly to administer, and safer than cryptocurrencies — or even common income.

“It continue to is a wild west clearly show and we need to have regulatory clarity to tame it,” claimed Avivah Litan, a distinguished analyst and vice president at investigate company Gartner. “Regulatory agencies have various sights on cryptocurrencies.”

For case in point, the US Securities and Trade Fee (SEC), the Commodity Futures Buying and selling Fee (CFTC), the Treasury and the Inner Revenue Services (IRS) are not unified in their definitions and regulatory therapy for crypto, and regulatory obligations and jurisdictions are not clear amid them (e.g. across/involving the CFTC and the SEC), Litan explained.

“There are also a number of competing initiatives in Congress for crypto-associated legislation, most of which have not passed,” Litan explained. “With any luck ,, the Executive Purchase will clarify the roles and how cryptocurrencies are treated heading forward.”

Of the countries or areas with the 4 premier central banking institutions — the US, the European Union, Japan, and the United kingdom — the United States is furthest behind, according to the Atlantic Council. And China has been increasing the pilot plan of its retail CBDC — the e-CNY — even though concurrently banning the use of cryptocurrency. Nigeria launched its CBDC, the e-Naira, in October 2021 for retail use.

“China, Thailand, the UAE, and many other countries are also exploring cross-border jobs, a testament to their curiosity in environment technologies and policy requirements internationally,” Kumar said in a weblog put up previous week.

One particular dilemma with the absence of worldwide specifications and regulatory oversight is that cryptocurrencies can be employed by legal teams for nefarious functions and rogue nations to bypass regular financial messaging networks. For illustration, faced with a expanding number of sanctions subsequent its invasion of Ukraine, Russia is probable utilizing cryptocurrencies to carry on cross-border commerce anonymously.

“To start out with, privateness and shopper security benchmarks are necessary,” Kumar explained. “Europe now prospects the planet with that and any person who wants to do commerce with them has to comply with individuals standards. It’s a extremely fragmented procedure at the moment, and that is where you require intercontinental bodies to build benchmarks that will work to your benefit.”

Electronic forex, which include cryptocurrencies, have found explosive development in modern decades, passing a $3 trillion sector capitalization last November (up from $14 billion just 5 years previously). Surveys counsel that all around 16% of grownup Americans — about 40 million people today — have invested in, traded, or employed cryptocurrencies. Extra than 100 nations are exploring or piloting CBDCs, a electronic kind of a country’s sovereign currency.

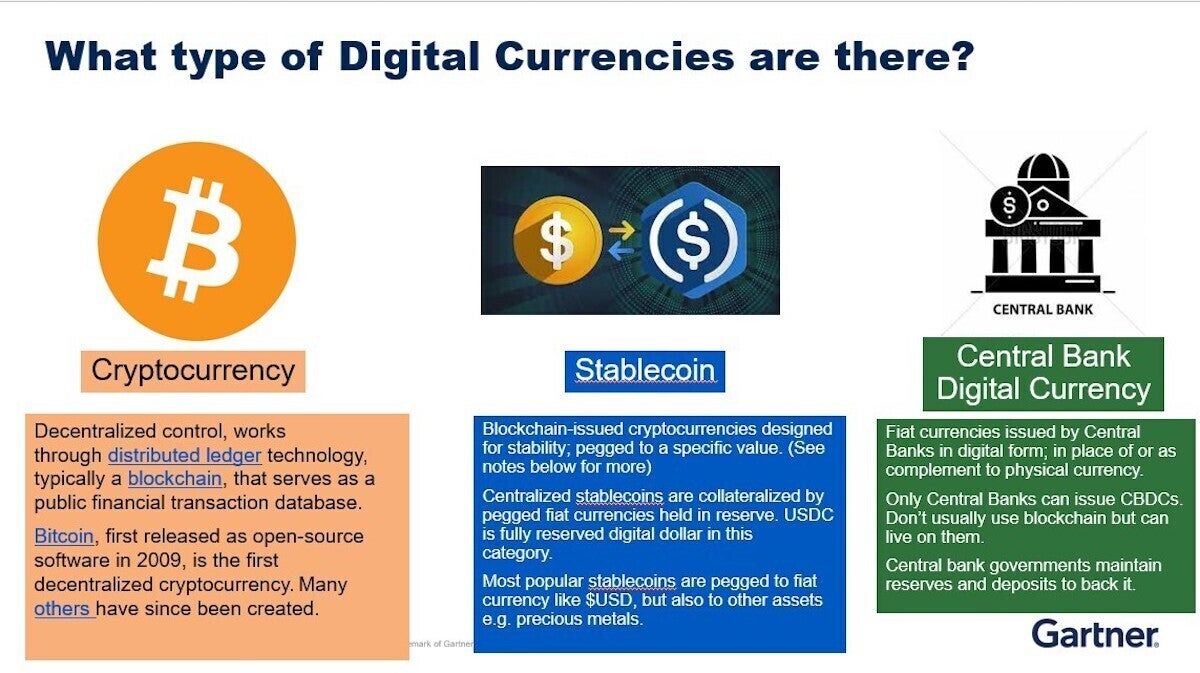

Usually talking, there are a few sorts of electronic currency:

- Cryptocurrencies, such as bitcoin and Ethereum, created and traded on blockchain dispersed ledger technological innovation (DLT)

- Stablecoin, this kind of as Tether and USD Coin, backed by fiat currencies like the US greenback

- Central Lender Digital Currency (CBDC), or fiat currencies issued by central banking companies in electronic variety and are not categorized as cryptocurrency.

Folks who get and sell electronic currencies use digital wallets that contain public and private encryption keys. The community keys are made use of to mail or get digital coins the personal keys aid ensure no a person can steal it from the holder, as only they maintain the code. The digital currency transactions are recorded via an online electronic ledger that in the scenario of CBDCs is usually managed by a central bank. In distinction, cryptocurrencies, these kinds of as bicoin, are transferred and tracked on a public electronic ledger known as a “blockchain,” which is taken care of by electronic currency “miners” or the men and women who use pcs to generate cryptocurrency.

Cryptocurrencies provide sellers and buyers anomymity via encryption, but that same encryption makes certain transactions are unchangeable or immutable.

There are, however, some CBDC assignments that use blockchain distributed ledger technological innovation (DLT) — the same know-how utilised by bitcoin and other community cryptocurrencies.

Sweden, for example, is screening a blockchain DLT for its digital currency, and those currencies can interact with other CBDCs. For instance China’s Digital Yuan can be transferred employing a bridge, gateway, or other interoperability protocol to a DLT/Blockchain “as they have carried out,” Litan reported.

Gartner

GartnerThree kinds of cryptocurrency.

Financial institutions have by now been piloting stablecoin as a process of cross-border payments to augment or switch standard monetary rails, these types of as SWIFT — the world’s greatest fiscal messaging network.

JP Morgan and Wells Fargo have piloted their very own stablecoin to tackle inner settlements with their business partners. Compared with cross-border transactions by means of regular settlement messaging networks, which can just take three days or far more to clear, cryptocurrency transactions are nearly instantaneous and there are no service fees.

Even prior to Biden’s govt buy, the US had been on the lookout at the development of a federally-backed digital dollar through Undertaking Hamilton, a collaboration amongst The Federal Reserve Financial institution of Boston and the Massachusetts Institute of Technology’s Electronic Currency Initiative (MIT DCI).

Challenge Hamilton’s reason is to create a CBDC design and style and get a fingers-on comprehending technological troubles and prospects. “Our major aim was to style a core transaction processor that fulfills the robust pace, throughput, and fault tolerance specifications of a big retail payment method,” the Project Hamilton’s executive summary states.

The Federal Reserve also not long ago published a CBDC plan paper it is now in the community comment stage until eventually May possibly 22.

Gartner

GartnerThese days, eighty-seven international locations (symbolizing additional than 90% of international GDP) are checking out a CBDC together with 45 central banks in Could 2020, just 35 nations were being thinking of a CBDC, according to the Atlantic Council.

Nine nations have previously launched a electronic forex. Nigeria is the most up-to-date with the e-Naira, the 1st CBDC outside the Caribbean.

At the very same time, 15 international locations have released CBDC pilot projects to take a look at the waters, such as China, Russia, Saudi Arabia and South Africa, Singapore, South Korea and Thailand. “China is a great deal even more along than the US, and about a yr ago tested a multi-nationwide dispersed ledger for cross-border payments with Thailand, the UAE, and Hong Kong,” Litan claimed.

In 2019, two of the largest economies in the Middle East, the United Arab Emirates and Saudi Arabia, introduced a bilateral CBDC pilot job called Venture Aber. The challenge concluded that DLT can properly facilitate cross-border transactions.

“The project was profitable in reaching its critical goals, which incorporate employing a new DLT-based option for authentic-time, cross-border interbank payments amongst professional banking institutions without having the have to have to maintain and reconcile Nostro accounts with every single other,” a multinational review concluded. “This guarantees to tackle the inefficiency and expenditures that are inherent in existing cross-border payment mechanisms.”

In February 2021, the United Arab Emirates joined China, Hong Kong, and Thailand in a joint CBDC cross-border exam. This “Multiple Central Bank Digital Forex (m-CBDC) Bridge” will check the use of DLT for overseas currency payments, the Atlantic Council stated.

With out world criteria and global coordination, having said that, any CBDC-based cross border payment devices could face significant interoperability troubles down the road, in accordance to the Atlantic Council.

Kumar mentioned the US desires to shift quickly if it would like to capture up to what other nations have been doing.

“The United States has not been focusing coordinated attempts on this, and this is the time that we commence contemplating about it extra very seriously than we have,” he stated. “Normally, we are heading to miss out on out on the purposes of this innovation. We’re likely to miss out on out on how this know-how is helpful and how regulated improvements can supply economical advantages for our culture. And, we’re going to miss out on out on more cost-effective, more quickly, safer payments.”

Copyright © 2022 IDG Communications, Inc.